Technology breakthroughs aren’t enough to solve American critical minerals challenges

But they can still move the needle in a big way, with the right federal support

This is the seventh post in my Tailings series. I’ll once again reiterate that these posts do not constitute financial advice. All companies mentioned are named simply to provide examples, and don’t reflect diligence performed or any other endorsement of their technology.

I said this week’s post would be much shorter on account of travel. I lied. Sorry. Let’s get to it.

Even if you’re entirely new to critical minerals, you’ve certainly seen the problem in your own line of work.

Some call it the “better mousetrap” problem, I prefer “shiny object syndrome.” But there are no shortage of engineers, financiers, policymakers, and enthusiasts who see a competitiveness deficit, and latch onto alternative speculative technologies as the sole or optimal solution. This group of people never seems interested in iterative process innovation, finding ways to improve performance, reliability, and cost competitiveness of existing products.

No material in the mineral insecurity realm illustrates this challenge better than graphite—both natural and synthetic. The material is virtually irreplaceable in lithium-ion batteries (for now), completely dominated by Chinese producers, and uneconomical for US production without incentives and/or protectionist trade barriers.

As a result, many…and yes, I’ve encountered this A TON…people in and around the battery sector have concluded that graphite is a lost cause, and America should look to the next, more advanced materials as substitutes. That means silicon anodes or, beyond that, lithium metal anodes in solid state batteries. I’m optimistic about both technologies over a longer time horizon, but would aggressively reject the assumption we can just give up on high-quality domestic graphite production. More on that momentarily.

Similarly, we see many too-good-to-be-true solutions hawked for extracting or processing minerals more efficiently or unlocking entirely new classes of resources. I’m not in a position to throw stones at someone’s lab-stage intellectual property, but also recognize the overwhelming majority of these technologies, however promising, are still many years from commercial readiness—if they reach it at all.

Technological innovations are inevitably part of the solution, but we should also be cognizant that addressing risks in the short-to-medium term will also involve brute forcing our way through problems via subsidies for less-economic production, or other market interventions that buy us time for longer-term alternatives.

The breakthroughs we seek

Technology innovations can help us tackle minerals security challenges in three areas:

Exploration and extraction

Processing

Product substitution

The first two are pretty straightforward. Someone develops technology that helps us identify and scope mine assets far better than we’ve been able to, cutting the cost and time needed to complete exploration and feasibility work. Or technology that helps us extract a purer and more economical product directly from the resource. Or technology that sits in the midstream refinery, and meaningfully reduces the cost of separating minerals from ore concentrate, brine, or other unrefined material.

The graphite problem I laid out is a good example of product substitution, whereby a breakthrough in silicon anode production may allow cost-effective replacement of some graphite in battery anodes. Many cellmakers already mix in small quantities of silicon, mostly to enhance charging performance, and technology breakthroughs are more likely to increase their proportion of anode content versus displace graphite entirely. The extent of replacement will likely depend on performance requirements in different market segments.

I’d also differentiate between product substitution enabled only by real technology breakthroughs (no matter how transformative), and more readily attainable outcomes by trading cost or marginal performance differential for supply chain security. In some cases, it’s as simple as just being able to identify the material vulnerability in your supply chain, and then engineering it out.

Another oft-cited substitution opportunity is rare-earth free high performance magnets, such as the iron nitride products Niron Magnetics seeks to commercialize. Lower cost magnets that can match performance of even just the lower-end rare-earth-based chemistries would minimize some supply chain vulnerabilities. I’ll explain in greater detail why these particular technologies are unlikely to completely displace demand of status quo materials in my future posts on graphite and rare-earths.

In reality, there are very few “blue ocean”1 technology opportunities in mining and materials processing, owing to the diversity of mineral resources, market dynamics, and maturity/optimization we already see across different value chains.

This is an important distinction…because it limits where and how venture capital may be willing to engage in the sector, and that means we’ll need to mobilize more conventional corporate R&D to solve many of our problems. Or at least enlist/entice established industrial players into technology development as strategic partners. And those different pathways require different federal support mechanisms to foster innovation where beneficial.

I’d also argue that we need to step back and look at the broader set of critical minerals through a framework of where innovations can enhance US competitiveness or help us circumvent chokepoints, and those where we’ll simply need to find ways to reduce consumption or accept other market interventions to mitigate security risks.

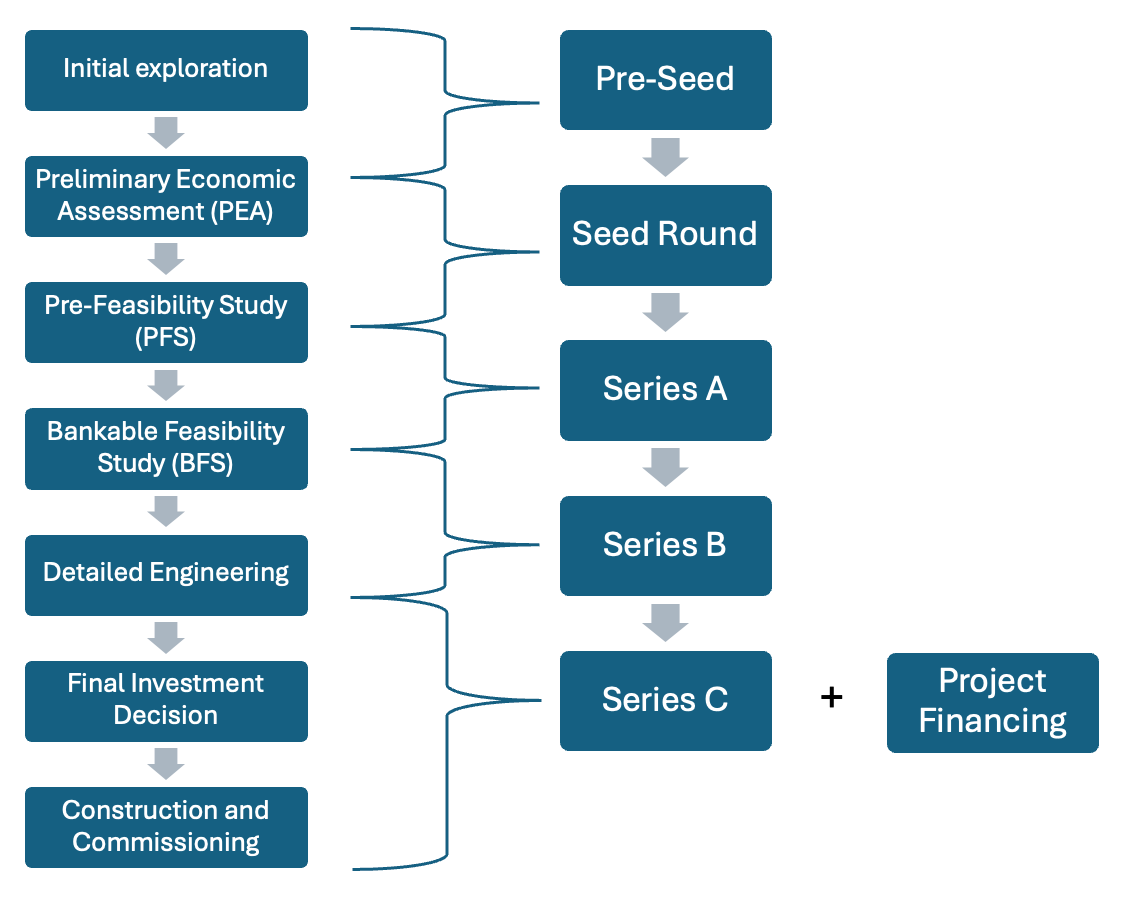

Bringing venture into mining

If you read my “How to build a mine” posts (or at least Part 2), then you might recall a schematic I shared comparing mine development to venture investing stages. If not, here it is again:

As I said then, it’s not a perfect comparison, especially because junior miners typically go public at very early stages, long before they have revenue. But venture capital does layer into the ecosystem as well, increasingly showing up as the primary financing pathway for most of these technology-driven solutions.

As with venture funding in other sectors, these solutions need to promise high degrees of scalability across multiple resources. This is why we tend to see them in the midstream processing stages, and also, if not targeting a large volume mineral (like copper or lithium), we tend to see them roadmap an ability to process many different critical minerals. See ReElement, or newer startups Valor and Mariana Minerals. As with exploration-oriented startup Kobold Metals, these newer entrants increasingly rely on promises of machine vision, robotics, and artificial intelligence to enable what the miners and metallurgists haven’t been able to achieve, and with unlimited customization.

I’ve seen other technology startups with more specific mineral focus, covering graphite, magnesium, gallium, and others, but some of the highest profile venture financing activity we’ve seen over the past 5-6 years concentrated around recycling and lithium. Why? Market size and domestic market opportunity.

Big promises, bespoke progress

Nonetheless, every one of these companies faces challenges around slotting into the value chain, with diverse geologies or mineral feedstocks that limit practical scalability of their products.

Developers of direct lithium extraction (DLE) technologies - which I plan to cover in my upcoming post on lithium - like to talk about the scalability of their solutions across many resources. But they ultimately require extensive technology refinement from one lithium mine to the next, and each technology certainly needs a strong anchor project just to prove viability at commercial scale.

My time at the Department of Energy (DOE) left me hopeful that DLE will ultimately help us tap America’s landscape of unconventional lithium resources, but these technologies aren’t well-suited to the venture funding model and its scalability expectations. I’m not saying the venture-backed startups will fail and their mature industrial competitors will succeed, but DLE looks more like a bespoke industrial product for each lithium resource than a plug-and-play catalyst of rapid growth. Without larger structural market changes, DLE is unlikely to unleash a fracking-style burst of new supply brought to market in rapid succession.

While not attracting the same degree of venture interest, copper’s market size and *extremely* challenging project development in the US (for both mines and smelters) created an opportunity for what may be that market’s DLE equivalent. And interestingly…incubated by one of the mining majors, not external venture capital. In December, Rio Tinto’s Nuton subsidiary began producing its first bio-leached copper in situ (i.e., processed in the ground), which could transform copper economics and increase domestic production of cathode without requiring new smelter capacity.

It’s not yet clear how the technology performs across different ores and mine designs, but for now at least, the technology appears supplemental where copper would otherwise be uneconomical to extract. That means the big money will continue to focus on conventional mine development domestically, where we lack additional smelter capacity to process copper concentrates. And I’ve yet to see anyone come forward with a technology solution to atrocious project economics for a greenfield US copper smelter.

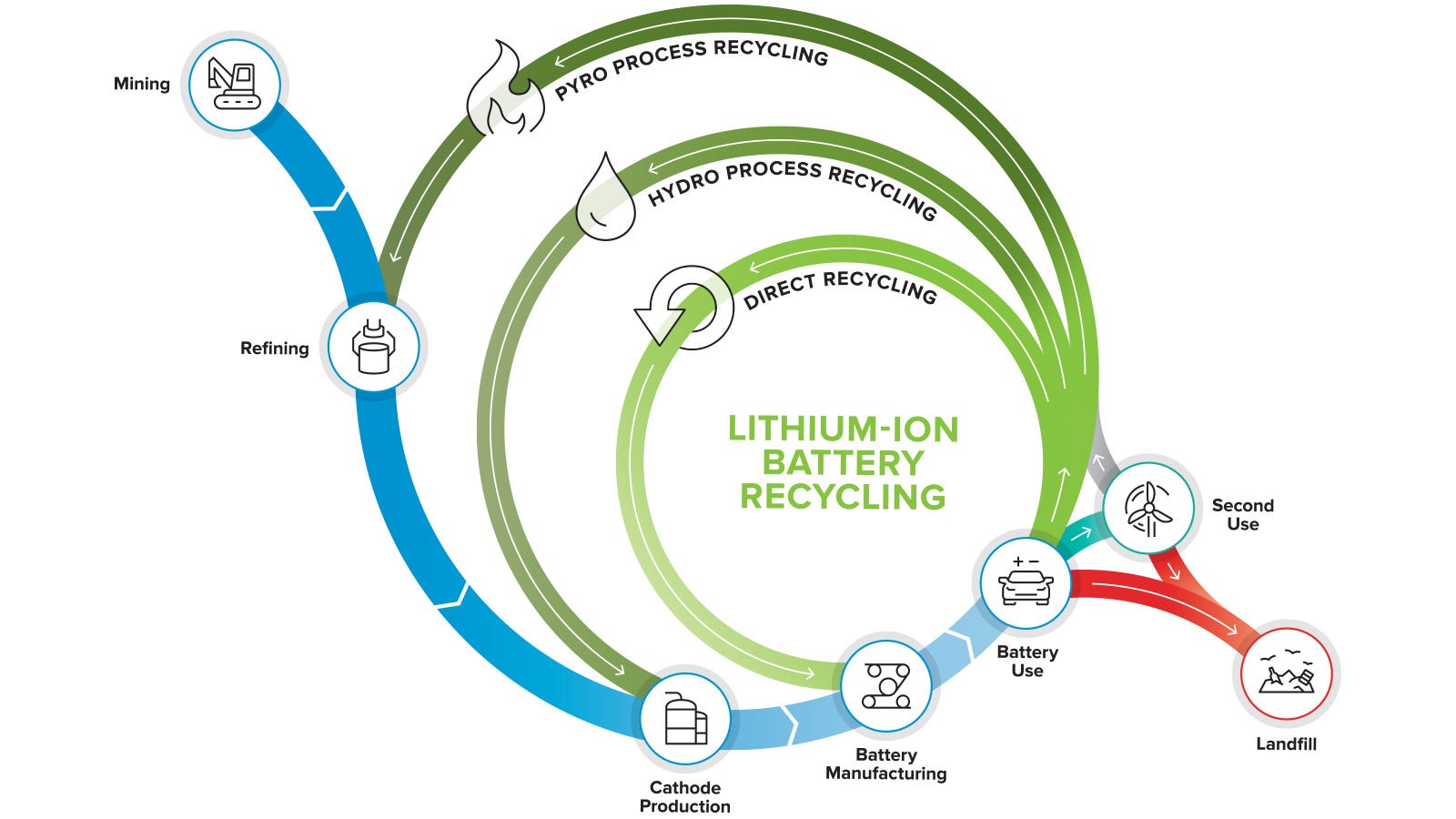

Finally, recyclers of batteries and e-waste often promise feedstock-agnostic solutions, but recycling economics say otherwise. These operations typically require large volumes of material containing high-value metals, and as with other recycling, over-engineer their lines around the expected presence of contaminating materials. These companies were able to raise large sums of venture funding in the early 2020s during the clean tech boom, promising rapid scalability alongside hockey-stick growth forecasts for recyclable feedstocks and surging metals prices.

While not rocket science, these companies all claim to leverage technology innovations allowing them to more efficiently process various battery feedstocks. In reality, hydrometallurgical processing (i.e., acid washing) has limitations. Battery market shifts, including slower demand growth and changing chemistry preferences2 have taken their toll on the sector outlook, forcing business model adjustments and calls for federal support to buffer operations until electric vehicles are retiring enough batteries to help domestic recyclers achieve economies of scale.

The common thread tying these examples together is the need for other market reforms, interventions, or natural evolutions to complement technology innovations for both mining and mineral processing. None are likely to achieve big “breakout moments” that create radically improved project economics overnight.

Fostering innovation

Federal support for critical minerals requires end-to-end support for both technology and resource-specific project development, which intersect but don’t necessarily advance in conjunction. DOE funding activities skew toward technology, especially at earlier stages of development, but ultimately require physical resources as testbeds for those technologies. And mining is a conservative industry where established players are structurally biased toward established practices with little incentive to risk innovations.

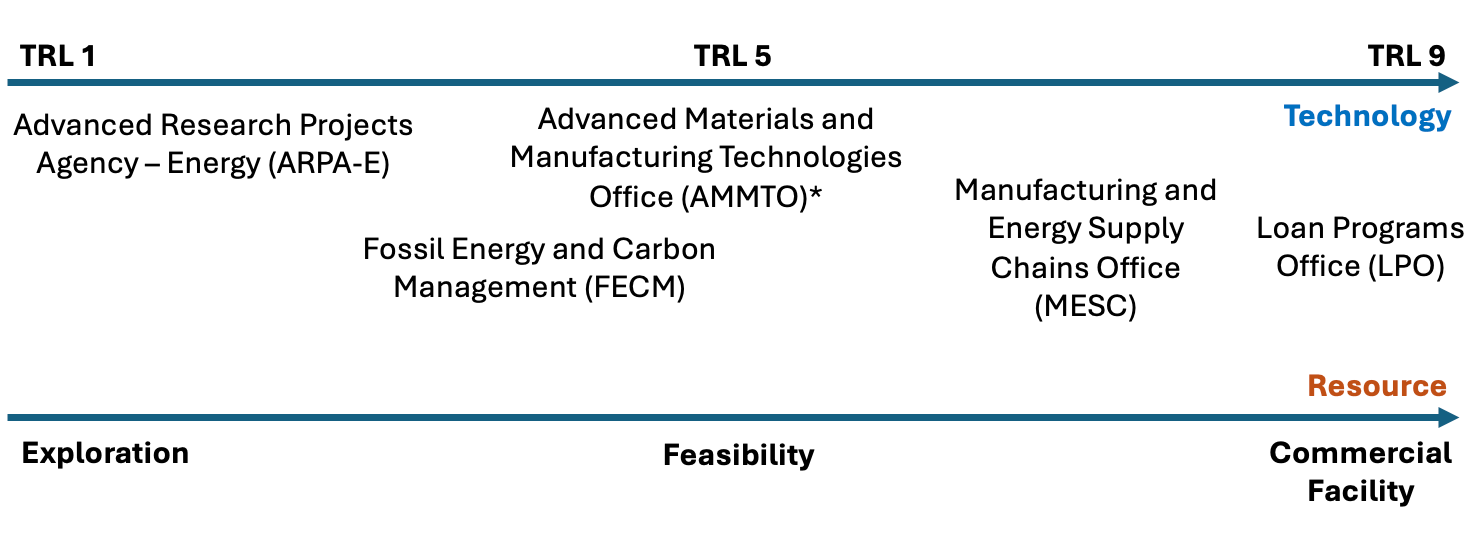

Earlier in 2025, I was helping some of my colleagues in a couple other DOE offices map out where they sit in the mining commercialization pathway, an exercise to help their new political leadership with strategic planning. I’ve provided a crude re-creation of what we conjured. Note that this isn’t a full representation of all DOE program offices with critical minerals funding opportunities, just its primary ones.

This schematic represents DOE prior to its November 2025 reorganization, which put what had been the Manufacturing and Energy Supply Chain Office (MESC) and most remnants of the heavily DOGE’d Energy Efficiency and Renewable Energy Office (EERE)3 all under a new roof. The new Office of Critical Minerals and Energy Innovation (CMEI) will now own responsibility for most grant funding and sector strategy outside the earliest stage breakthrough innovation, housed in ARPA-E, some specific mine resource programs4, and the Energy Dominance Financing Office (EDF) (née Loan Programs Office (LPO)).

The drive to orient DOE around commercialization, and not just R&D, was very much the product of the Biden Administration’s industrial policy vision. Agency leadership, supported by new programming funded under the Bipartisan Infrastructure Law (BIL) and Inflation Reduction Act (IRA), tried to structure a continuum of program funding covering the entire technology development lifecycle in many technology areas.

In theory, there was a program office for every Technology Readiness Level (TRL), from 1 to 9, though gaps emerged for mining and processing. I described the most glaring of these in last week’s post, where we lacked grant funding structured to support the pilot or demonstration plants needed to de-risk commercial scale-up.

But there were others.

Where DOE couldn’t bridge the gap

For critical minerals-oriented programming, we lacked adequate funding tools to advance the mine projects themselves, instead focusing primarily on the technology for processing. Which…makes sense. Ultimately, DOE is a technology agency, and had awkwardly assumed the primary role of supporting domestic mine projects during the Biden Administration. All while lacking the funding tools or flexibility to do so.

LPO sat at the end of that funnel, with every other office’s grant funding serving to derisk technologies and projects before they could ultimately seek debt financing for commercial scale-up. Most manufacturing or supply chain projects at LPO involved some innovative technology, even though we generally didn’t take technology risk. Our charge was to finance TRL 8 or 9 projects (in rare instances, TRL 7) that featured degrees of market or other commercial risk.

We collaborated with colleagues in other offices to infuse more commercial orientation into their grant programs for earlier stage projects, but the tools available to them were generally inadequate in scale and flexibility. Mostly because these programs mirrored R&D funding in other sectors, with more generically scalable and less bespoke market applications. In other words, these worked fine for companies seeking seed or other early stage venture funding in relevant technology areas (like recycling), but less so for resource-specific technology development.

The Fossil Energy and Carbon Management Office (FECM) had some smaller funding programs (i.e., $2-3 million awards) that could partially fund feasibility studies on mines, but they were structured as any other multiyear R&D grant with technical milestones. These were awkward fits, often tied to specific technology areas of DOE’s choosing*, too infrequent for mining companies to plan around, and simply didn’t align to industry project development timelines.

*Sometimes these directions come directly from Congress in authorizing/appropriating statute, another problem I’ll discuss in a subsequent post.

As such, most of the funding ended up supporting science projects with mine tailings and other waste streams, or highly speculative “host” developers willing to partner with researchers on snag small grants for resources with poor commercial prospects. And no buy-in from major industry stakeholders. I see merit in funding standalone technology development, but we also need funding that allows more formidable mine developers to advance innovative technologies alongside their commercial project. And ensure those projects can demonstrate market relevance.

My colleagues at FECM (now under HGEO) spent the past several years developing their recently-launched “Mine of the Future” initiative that potentially addresses some of these disconnects. The program is still technology-focused, but offers larger grant awards to entice commercially-focused projects as prospective applicants. If successful, we’ll see projects that enable technology and mine development symbiotically. Funding levels are woefully inadequate at launch, but could nonetheless serve as a foundation for program scale-up with subsequent appropriations.

Drawing back on my prior comparison of private funders, programs like these lend themselves more to corporate R&D, bolting promising technologies onto existing project development to solve specific problems—not the venture-style “blue ocean” mindset. Given project development timelines, financier risk appetite, and mine lives once in operation, we simply don’t have many opportunities to embed major innovations in projects. Mine plans tend to stick for life.

I’m hopeful that the reorganized DOE is better suited to support mining projects from inception through construction, with innovation improving American competitiveness against global alternatives. However, the Trump Administration has thus far shown little interest in incubating earlier stage projects given its orientation toward dealmaking and quick wins, and I could also see much of this necessary programming languish until a subsequent administration picks it up.

Final thoughts

I didn’t address electrification and surface automation technologies (e.g. automated trucks) here because I see these as helpful on the margins, but likely not the sort of breakthroughs that unlock new resources. Other technology oriented toward industrial efficiency may also help processing plant operations, but have much broader commercial applications and are too broad to discuss in this series.

I also didn’t include it in my schematic, but the Department of Defense’s (DOD) Industrial Base programs, including Defense Production Act (DPA) Title III, had greater flexibility and ultimately impact to project development over the past few years. I would often refer projects seeking feasibility study support to DOS programs, since DOE lacked the tools to effectively serve those projects. I don’t think DPA should be the longer-term tool for commercial projects not specifically tied to the defense industrial base, but until policymakers streamline funding programs, developers will (and should) continue to lean on it.

I’m not an expert on innovation policy, and won’t pretend to be. Someone else needs to conjure the grand vision for reorganizing the way we incubate promising technologies and increase their likelihood of commercialization. But we do need to better tie federal R&D programming to commercial objectives, even while reserving a place for “science for science’s sake.” I found many of the grant programs in DOE’s R&D-oriented offices too detached from commercial objectives, feeding niche research favoring certain political constituencies (e.g., fossil fuel producing regions) or what amounted to make-work for the national labs.

Next week I’ll dive back into financing topics, starting with the corporate/project capital stack and government tools to support capital formation. See you then.

For those unfamiliar with the venture terminology, “blue ocean” refers to a technology or product innovation seen and marketed (often incorrectly) as having near limitless market potential.

The shift from nickel-based lithium-ion battery chemistries to lithium iron phosphate challenges recycling economics, since iron and phosphorus are dirt cheap compared to the nickel and cobalt they replace.

EERE included many sub-offices dedicated to different energy technologies. The Advanced Materials and Manufacturing Technologies Office (AMMTO) had primary responsibility within EERE for mining and minerals processing technologies, but others including the Geothermal Technologies Office (GTO) and Vehicle Technologies Office (VTO) had some programming supporting critical minerals as well.

Most of the Fossil Energy and Carbon Management Office (FECM) programming appears to have been reorganized under the Hydrocarbons and Geothermal Energy Office (HGEO).